Yield to Call (YTC)

What Is Yield to Call (YTC)? A Detailed Explanation

Yield to Call (YTC) is a measure of the potential return on a callable bond if it is called (redeemed) by the issuer before its maturity date. Callable bonds give the issuer the option to redeem the bond early, usually after a certain period, at a specified call price (often at par or slightly above par). YTC calculates the yield assuming that the bond will be called at the earliest possible date, which could be advantageous to the issuer if interest rates decline.

YTC is similar to Yield to Maturity (YTM), but instead of assuming the bond will be held until maturity, it assumes the bond will be called at the first opportunity. Investors often use YTC to evaluate the potential return on callable bonds when they are uncertain whether the bond will be called early or held to maturity.

Understanding Yield to Call (YTC)

Callable bonds are issued with a call provision that allows the issuer to redeem the bond before the maturity date, typically after an initial call protection period. This option is beneficial to issuers because, in a falling interest rate environment, they can refinance their debt at lower rates by calling the bond and issuing new bonds at a lower interest rate.

However, the call option also exposes investors to the risk that the bond might be called early, which would cut short their expected returns. When a bond is called early, the investor may not be able to reinvest the principal at the same interest rate, potentially leading to lower returns. YTC helps investors determine the yield they would receive if the bond were called at the earliest date.

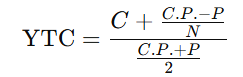

How to Calculate Yield to Call (YTC)

The formula for YTC is similar to the calculation for YTM, but instead of the bond’s maturity date, it uses the bond’s call date and call price. The calculation involves finding the interest rate (YTC) that equates the present value of the bond’s future cash flows (coupon payments and the call price) to its current market price.

The formula is:

Where:

C = Annual coupon payment

C.P. = Call price (the price at which the issuer can call the bond)

P = Current market price of the bond

N = Number of years until the bond can be called (time to the call date)

The calculation involves solving for the interest rate (YTC) that satisfies the equation, given the coupon payments and the call price. Most investors use a financial calculator or spreadsheet software to perform this calculation due to its complexity.

Why Is Yield to Call Important?

YTC is a critical measure for investors considering callable bonds because it provides insight into the bond's potential return in the event it is called early by the issuer. Understanding YTC can help investors assess the risks and rewards associated with callable bonds and make more informed investment decisions. Here's why YTC matters:

Callable Bond Risks:

Callable bonds expose investors to the risk that the bond may be called early, particularly in a falling interest rate environment. If the bond is called early, the investor may have to reinvest the principal at a lower interest rate, reducing the overall return. YTC helps investors evaluate this risk by showing the potential return if the bond is called early.

Comparing Callable Bonds:

YTC is useful for comparing callable bonds with other bonds, whether callable or non-callable. Since callable bonds offer higher yields to compensate for the call risk, YTC provides a clearer understanding of the potential return considering the likelihood of the bond being called.

Issuer Incentives:

Issuers are more likely to call a bond when interest rates fall because they can refinance their debt at a lower cost. By calculating the YTC, investors can gauge how the bond’s return compares to other bonds and the prevailing interest rate environment. If interest rates are expected to fall, the likelihood of a call increases, and investors should consider the YTC as a more realistic measure of return than YTM.

Investment Decision-Making:

YTC helps investors assess whether a callable bond offers an attractive return, considering the likelihood of the bond being called early. If the bond is called early, the investor may receive less than the expected YTM. Therefore, by analyzing YTC, investors can better assess whether the bond fits their investment strategy.

Factors That Affect Yield to Call (YTC)

Several factors influence YTC, as they impact the likelihood of the bond being called early and the potential return an investor might earn:

Interest Rates:

The most significant factor affecting YTC is the prevailing interest rate environment. If interest rates fall, issuers are more likely to call their bonds early to refinance at a lower rate. A drop in interest rates increases the likelihood of the bond being called, which may lower the actual return for the investor.

Call Price:

The call price is the price at which the issuer can call the bond, and it is often specified in the bond’s terms. The call price may be higher than the face value, especially if the bond has a premium call option. The call price can affect the potential return on the bond if it is called early.

Time to Call:

The time to call is the number of years until the bond can be called. The shorter the time to call, the more likely the bond is to be called if interest rates decrease. Bonds with shorter call protection periods are more susceptible to being called early, which could lower the overall return for the investor.

Coupon Rate:

The coupon rate is the annual interest paid to the bondholder, and it influences the attractiveness of the bond. If the coupon rate is higher than the current market interest rates, the bond is less likely to be called early because the issuer would prefer to keep paying the higher coupon rate. Conversely, if the coupon rate is lower than current market rates, the issuer is more likely to call the bond.

Bond Rating:

The credit quality of the issuer can also affect the likelihood of the bond being called. Issuers with higher credit ratings are less likely to call bonds early, as they may have better access to capital markets and lower borrowing costs. However, issuers with lower credit ratings may be more inclined to call bonds if they can refinance at a better rate.

Yield to Call vs. Yield to Maturity (YTM)

It’s important to distinguish between YTC and YTM, as they are both measures of a bond's potential return but are based on different assumptions:

YTM assumes that the bond is held until maturity, and it factors in the bond’s coupon payments and the face value repayment.

YTC assumes that the bond will be called at the earliest possible date, which may be before maturity, and it factors in the bond’s coupon payments and the call price.

YTC is generally lower than YTM for callable bonds because it assumes the bond will be called before maturity, which limits the amount of time the bondholder will receive interest payments. YTM, on the other hand, assumes that the bond will be held to maturity, which could result in a higher return if the bond is not called early.

Conclusion

Yield to Call (YTC) is an important metric for investors evaluating callable bonds, as it measures the potential return assuming the bond is called at the earliest opportunity. Since callable bonds expose investors to the risk of early redemption by the issuer, YTC helps investors understand the bond’s expected return under this scenario, considering both coupon payments and the possibility of capital gains or losses. By assessing YTC, investors can make more informed decisions about whether callable bonds fit their investment objectives, especially in relation to changing interest rates and call provisions.